.webp)

Matthew Oliver

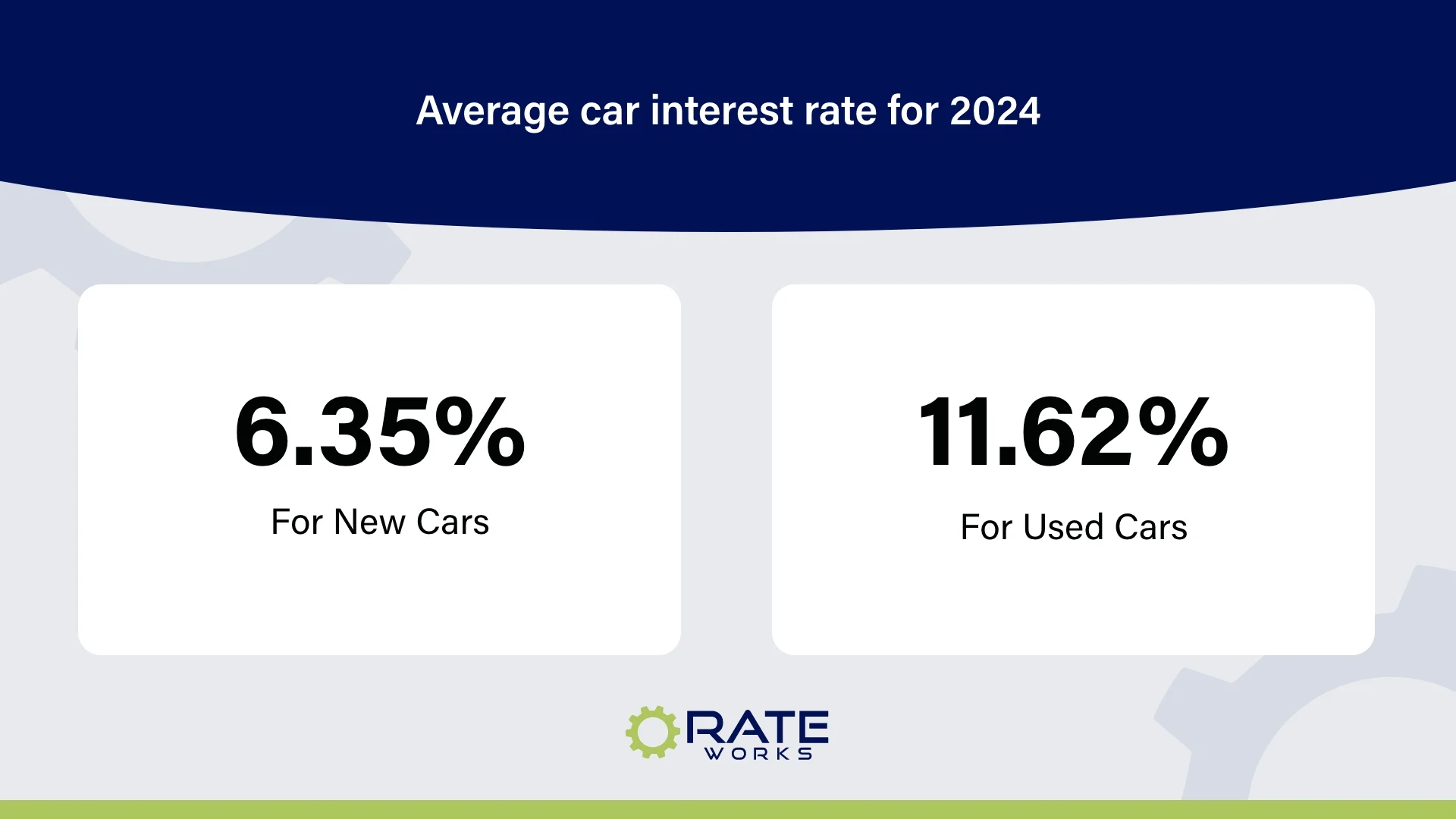

2025 has been an interesting year so far. We think we can all agree on that, especially when it comes to the economic landscape. We’re talking continued inflation, debt that continues to rise, and let’s not forget the recently imposed tariffs that are leading to national and geopolitical uncertainty. With all of this going on, it’s no wonder that car buyers are scratching their heads over interest rates. In fact, the average car interest rate for 2024 was 6.35% for new cars and 11.62% for used cars. But that’s not the case in 2025. In this article, we’ll tell you what you need to know.

What’s the Current Average Rate in 2025?

It can be frustrating when interest rates go up year after year. And it can be especially frustrating that interest rates go up just when the time comes for you to purchase a new or used vehicle. How are you supposed to predict that interest rates will be higher than ever when the time comes to replace your existing vehicle? Unfortunately, it’s just the reality.

So, just what are the average car interest rates for 2025? Check out this handy grid we have created below.

Source: https://cars.usnews.com/cars-trucks/advice/average-auto-loan-interest-rates

As you can see, interest rates are higher for both new and used cars, And your credit score plays a serious role in determining how much you’ll pay. Consider that the average credit score in the U.S. is currently around 715. If you look at our table above, that means that you’ll be paying 11.75% for a new car loan this year compared to an interest rate that might have been as low as 6.35% just last year. That can make a serious impact on how much you’ll pay over the course of your loan, not to mention your minimum monthly auto loan payment.

Rate Trends & National Context

Let’s be honest. Trying to follow the news day after day and stay on top of interest rates can be not just frustrating, but overwhelming to say the least. And every time the Fed makes a move, headlines start showing up on the nighttime news, in our newspapers, and even on social media. But what do those headlines and the Fed’s decisions really mean for your car loan? The answer is, a lot.

The Federal Reserve, aka the Fed, raises what is called the benchmark interest rate. And no, that doesn’t directly impact your auto loan rate, but it does affect how much it costs for banks to lend money to each other. So, when that cost goes up, banks and lenders will pass on some if not all, of that expense to consumers. That means you.

Simply said, the Federal Open Market Committee (FOMC) doesn’t set your specific car loan rate. But the decisions they make will have a trickle-down effect on what you will pay. The higher the benchmark rate from the Fed means the higher likelihood that your auto loan rate will go up.

Plus, there are other factors that impact the average car interest rate that you’ll pay in 2025.

- Time of year for your car purchase

- Whether you’re buying a new or a used car

- Your credit score (the higher your credit score, the more favorable your auto loan will be)

- The length of your loan and your specific loan terms

- The lender’s internal guidelines and policies

The bottom line? It’s not your imagination that auto loan interest rates are going up in 2025.

How This Helps You: Practical Takeaways

We’re not sharing this information to give you bad news or to discourage you from buying a car. We all need safe and effective transportation that can get us where we need to go. But, we’re hopeful that this information will help you make the best decision for you on when it’s the best time to purchase a new car or to refinance your existing car.

Here are some tips that we hope you can take away from this article.

- Use the average APRs we have shared as benchmarks. They may or may not be what you will actually pay.

- Know your credit score and take steps to improve it. As we said before, the higher your credit score, the more interest rates will work in your favor.

- Don’t settle for the first loan offer you see. Even car dealers will offer you multiple options. Do your homework and always read the fine print.

- Consider prequalification options. This can give you a better idea of the interest rate you will qualify for and what your monthly payment will be.

- If your car has been well-maintained and can live another day, consider auto loan refinancing. These rates are typically lower than what you will get on your initial loan and can save you some serious cash over the course of your loan.

Save on the Average Car Interest Rate in 2025 With Auto Loan Refinancing

Car buying today comes with more challenges than we might want to admit. But it doesn’t make it impossible. Simply stay on top of the trends, pay attention to your credit score, and compare offers to make the decision that is best for you. And if buying a new or new-to-you car isn’t in the cards now, an auto loan refinance with RateWorks may be the better option. We’re here to help you lower your monthly payment and save money over the course of your loan. Get a free quote today.